Section 43B(h) Explained: How Suppliers Can Recover Late Payments

Section 43B(h): What Indian Manufacturers Need to Know About Getting Paid on Time

If you are a Micro or Small Enterprise registered on the Udyam portal and your buyers are taking 60, 90, or 120 days to pay you, the law changed in your favour in April 2024.

Section 43B(h) of the Income Tax Act, 1961, introduced through the Finance Act 2023, now makes it a tax compliance matter for your buyer to pay you on time. If they do not, they lose the ability to deduct that expense from their taxable income in the current financial year.

Most suppliers do not know this. And most buyers are counting on that.

This article explains what the law says, what it means for your business, and how to use it practically without damaging the relationships that matter to you.

What Section 43B(h) Actually Says

Section 43B of the Income Tax Act, 1961 is the provision that governs which expenses a business can deduct from its taxable income. Before April 2024, most expenses could be deducted in the year they were incurred, regardless of when payment was actually made.

Clause (h), added by the Finance Act 2023 and effective from April 1, 2024 (Assessment Year 2024-25 onwards), creates a specific exception for payments owed to Micro and Small Enterprises registered under the Micro, Small and Medium Enterprises Development Act, 2006.

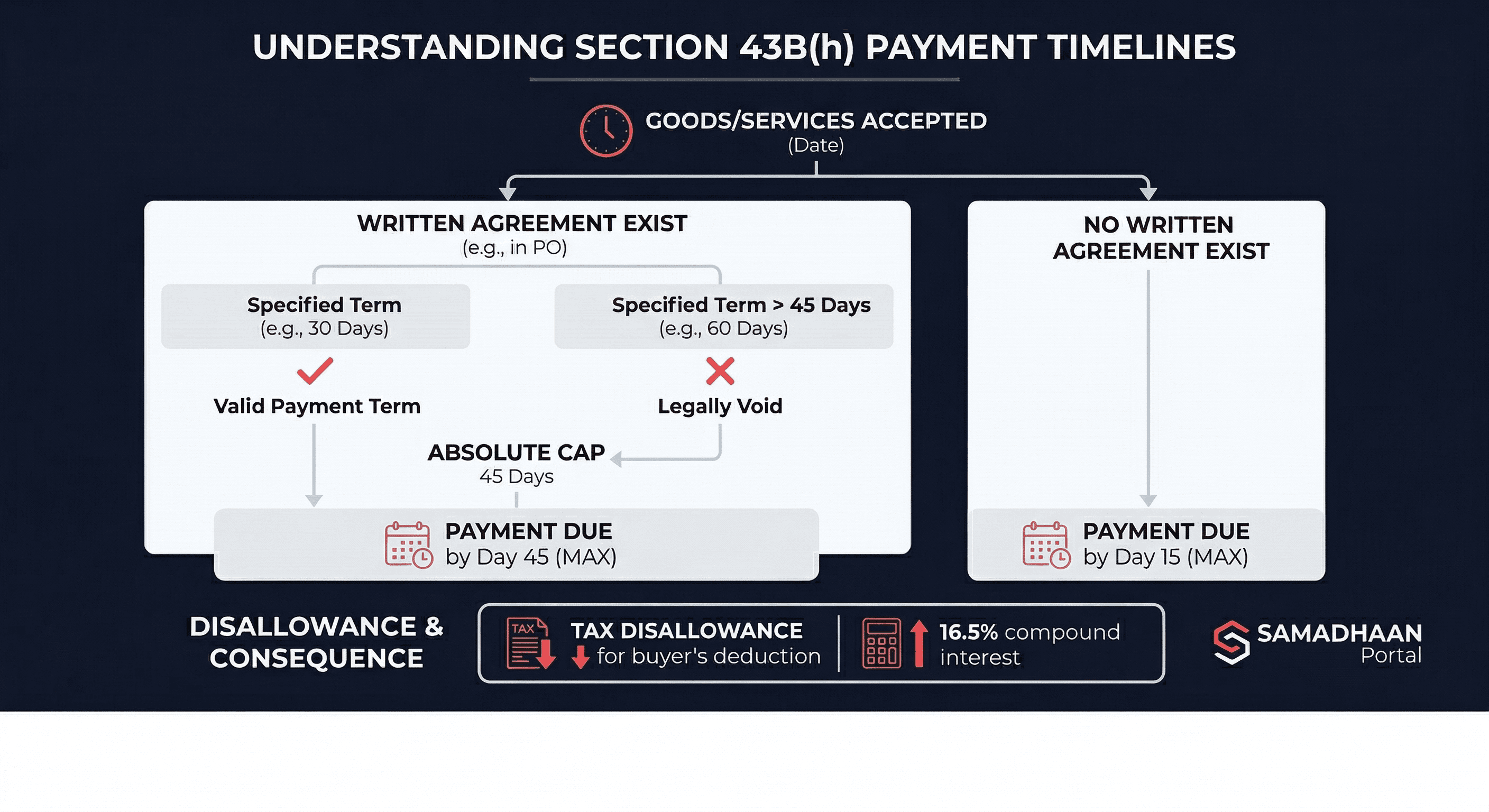

The rule is clear: if a business purchases goods or services from a registered Micro or Small Enterprise and does not pay within the time limits set by Section 15 of the MSMED Act, that expense cannot be claimed as a tax deduction in the year the goods or services were received.

The critical cut-off reality: The deduction shifts to the financial year in which the payment is actually made. If a buyer pays late during the year but clears the balance by March 31, they still get the tax deduction. The real tax consequence hits when the invoice is still unpaid as the financial year ends.

The 15-Day and 45-Day Rules

The payment timeline depends on whether there is a written agreement between you and your buyer.

No written agreement: Your buyer must pay within 15 days of accepting your goods or services. This is the strict default.

With a written agreement: Your buyer must pay by the date specified in the agreement, but that period cannot exceed 45 days from the date of acceptance. Any written agreement specifying a payment period longer than 45 days is legally void for this purpose. The 45-day cap is absolute.

A common misunderstanding: some buyers sign contracts specifying 60 or 90-day payment terms, believing this protects them under Section 43B(h). It does not. The law caps the allowed period at 45 days regardless of what the contract says.

Who This Applies To

For the rule to apply, two conditions must be met.

First, you, the supplier, must be registered under the MSMED Act via the Udyam portal as a Micro or Small Enterprise. Medium Enterprises are not covered by Section 43B(h) for this purpose.

Second, you must be a manufacturer or service provider, not a trader. Wholesale or retail traders registered on Udyam for lending purposes (Priority Sector Lending) are excluded from the delayed payment benefits of Section 15.

Your buyer does not need to be MSME-registered. The rule applies to any business purchasing from you, whether a large private company, a listed corporation, or another MSME, as long as you are Udyam-registered.

What Happens When a Buyer Delays Payment

Beyond the tax disallowance, delayed payment also triggers interest under the MSMED Act.

The interest rate is compound interest at three times the Reserve Bank of India bank rate. As of April 8, 2026, the RBI bank rate is 5.50%, making the applicable interest rate 16.5% per annum. This interest begins accruing from the day after the due date, automatically, without any action required from you.

Critically, this interest is not tax-deductible for your buyer. They cannot claim it as a business expense. This makes delayed payment genuinely expensive for them, not just a working capital convenience at your expense.

The Reality on the Ground

Despite this law being in effect since April 2024, delayed payments remain widespread.

According to official data placed before the Lok Sabha in July 2025, over Rs 22,363 crore in disputed delayed payments were pending resolution on the government's MSME Samadhaan portal. Over 2.18 lakh complaints had been filed since the portal's inception.

The law exists. The enforcement is incomplete. Many suppliers do not know their rights. And some buyers have found a workaround: a significant number of MSMEs cancelled their Udyam registration after the rule came into effect, often under pressure from large buyers who made it clear they would prefer to deal with unregistered suppliers who cannot invoke the rule.

How to Use This Law Practically

Step 1: Confirm your Udyam registration is current

Check your registration status at udyamregistration.gov.in. Your classification (Micro or Small) must be current for the provision to apply.

Step 2: Get your agreement in writing

If you do not have a written agreement, you have 15 days from acceptance. Get a simple written purchase order that specifies payment terms up to 45 days. This gives you documentation for any dispute.

Step 3: Track "Deemed Acceptance" dates

The clock starts from the date of acceptance. If the buyer does not object within 15 days of receiving the goods, they are deemed accepted. Always keep your Proof of Delivery or Inward Gate Pass copies to verify when the goods hit their floor.

Step 4: The Gentle Nudge

A written reminder three to five days before the due date creates a paper trail. If payment slips, send a Balance Confirmation request. When a buyer's auditor sees an unpaid balance over 45 days old, they may force the finance team to pay to avoid a qualified audit report.

Step 5: Know your escalation options

If payment is not made, you can use the MSME Samadhaan portal. The process is online and does not require a lawyer to initiate. Alternatively, you can raise the matter with your buyer's finance team, referencing Section 43B(h) directly. Many finance teams respond faster when they understand the tax consequence for their own organisation.

What About the Relationship?

This is the real concern for most suppliers. You need this buyer. Invoking legal rights against them feels like a risk.

The practical answer is to use the law as information, not as a threat.

At the point of signing an agreement, explaining the payment terms in the context of Section 43B(h) is not confrontational. You are informing the buyer of a compliance requirement they should be aware of. A good buyer's finance team will already know this rule and will appreciate a supplier who understands it.

What Section 43B(h) gives you is not a weapon. It gives you a reason to have a direct conversation about payment timing that does not need to feel personal. The law creates the context. You use that context to get paid.

What Section 43B(h) Does Not Do

It is important to be clear about the limits of this provision.

It does not guarantee fast payment. It creates a tax incentive for timely payment and a legal process for recovery. Neither is instant.

It does not apply to Medium Enterprises. If your Udyam registration classifies you as Medium, you are not covered by this specific clause.

It does not apply to traders. If your business activity is primarily wholesale or retail trading, the provision may not apply.

It does not override a dispute about the goods or services. If your buyer claims there is a defect, that dispute may toll the timeline. Get your quality documentation in order before raising a payment dispute.

The Broader Picture

Rs 22,363 crore in disputed delayed payments sitting on a government portal is not a compliance story. It is a working capital story. Every rupee of delayed payment is a rupee that a small manufacturer cannot use to buy raw materials, pay wages, or invest in capacity.

Section 43B(h) was designed to change the calculation for buyers. If delaying payment increases your tax liability and triggers 16.5% compound interest, the cost of delay becomes visible and immediate.

Whether it changes the culture of delayed payment in Indian manufacturing depends on how many suppliers know the rule exists and are willing to use it.

Download

Late Payment Recovery Tracker

XLSX · 27.4 KB

A tracker for Udyam-registered suppliers to monitor invoice dates, payment deadlines under Section 43B(h), interest accrued on delayed payments, and dispute status for each buyer.

Frequently asked questions

What is Section 43B(h) and why does it matter for small suppliers?

Section 43B(h) is a clause in India's Income Tax Act, introduced by the Finance Act 2023 and effective from April 1, 2024. It states that businesses buying goods or services from Udyam-registered Micro or Small Enterprises must pay within 15 days (if no written agreement) or 45 days (if there is an agreement) to claim that expense as a tax deduction. If they delay, the deduction is lost until they pay. This gives small suppliers a formal, tax-backed mechanism to encourage timely payment.

Does this law apply to all MSMEs?

No. It applies only to Micro and Small Enterprises registered under the Udyam portal. Medium Enterprises are not covered. Traders are also excluded - the rule applies to manufacturers and service providers only.

What interest can I charge on a delayed payment?

Under the MSMED Act, you can charge compound interest at three times the RBI bank rate from the day after the payment was due. As of April 2026, this works out to 16.5% per annum, compounded. This interest is not tax-deductible for the buyer.

Will invoking Section 43B(h) damage my relationship with the buyer?

Not if it is framed correctly. Referencing the legal payment timeline at the point of agreement - before an order is placed - is informing the buyer of a compliance requirement, not making a demand. Most finance teams in larger companies are already aware of this rule. A supplier who understands it is easier to deal with, not harder.

What if the buyer disputes the invoice or claims the goods were not acceptable?

A genuine quality dispute may toll the payment timeline - the clock may not start until the dispute is resolved. This is why maintaining quality documentation, delivery records, and written acceptance confirmation matters. A dispute that arises conveniently after a payment deadline should be treated carefully and documented.

How do I file a complaint on the Samadhaan portal?

Visit samadhaan.msme.gov.in. You will need your Udyam registration number, the buyer's details, copies of invoices, and documentation showing the acceptance date of goods or services. The complaint is forwarded to the relevant MSEFC for mediation or arbitration.

Ready for fewer, better conversations?

Augmino connects verified Indian manufacturers with buyers who mean business.

Apply to Join