CBAM for Indian Exporters: What the EU Carbon Border Tax Costs You and How to Avoid the Default Value Penalty

If you export steel, aluminium, cement, fertilizer, or hydrogen to the European Union, the most expensive number in your next shipment may not be your price. It may be a carbon figure you never calculated, assigned to you because you could not provide one of your own.

The EU's Carbon Border Adjustment Mechanism, CBAM, hit its definitive phase on January 1, 2026. Most people call it a carbon tax. That is true enough, but it misses the part that actually costs Indian exporters money. CBAM does not really charge you for your carbon. It charges you for not being able to prove your carbon. Document your real emissions and you pay on your real number. Fail to, and the EU assigns you a default value that assumes you run the dirtiest process in your category, and that default is set to climb every year.

So this is less a tax problem than a paperwork problem. Below is what CBAM covers, what the default value costs when it lands on you, and what to actually do about it before your buyer asks.

What CBAM actually does

European factories already pay for their carbon under the EU Emissions Trading System. CBAM exists so that imported goods carry the same cost, which stops EU buyers from simply sourcing the dirty stuff from outside the bloc to dodge the price. When you ship a covered product into the EU, the carbon burned making it now gets a price at the border.

It ran as a reporting-only trial from October 2023. The real version, with money changing hands and mandatory third-party verification, started on January 1, 2026.

The dates get muddled in a lot of coverage, so here they are straight. The reporting and data obligations are live right now. Importers cannot actually buy CBAM certificates until February 1, 2027. The first bill comes due on September 30, 2027, and it covers everything imported across 2026.

The key dates an exporter should hold in view:

| Date | What happens |

|---|---|

| Jan 1, 2026 | Definitive phase begins. Emissions on EU-bound goods now carry a cost. Verification becomes mandatory for actual-data claims. |

| Through 2026 | Your EU buyer needs verified emissions data for goods shipped this year. Measurement must happen at production. |

| Feb 1, 2027 | EU importers can begin buying CBAM certificates through the central platform. |

| Q1 2027 onward | Importers must hold certificates for at least 50% of emissions to date at each quarter-end. |

| Sep 30, 2027 | First annual declaration and certificate surrender, covering all 2026 imports. |

For the Indian exporter this distinction does not buy much time. The verified emissions data your EU buyer will need has to be generated at the point of production, which means the measurement work starts now regardless of when the certificate payment falls due.

What CBAM covers

Six categories are in scope: iron and steel, aluminium, cement, fertilizers, hydrogen, and electricity, plus a long list of upstream and downstream products within them. What counts is the customs code, not the general description, which matters more than it sounds like it should.

Check one thing before you assume CBAM applies to you at all. Since October 2025, under the Omnibus simplification rules, any importer bringing in 50 tonnes or less of CBAM goods a year is fully exempt. The Commission's own number is that this clears about 90% of importers, mostly small and mid-size firms, while still capturing 99% of the emissions that matter. Electricity and hydrogen do not get this exemption; they are in scope at any volume. So if your EU buyer takes only small quantities of your product, find out where they sit against that 50-tonne line before treating any of this as urgent. The threshold also gets reviewed each year, so it can move.

If your buyer is above the line, whether your specific product is caught comes down to its CN (Combined Nomenclature) code. Pull the exact code for what you ship and check it against the CBAM goods list. That is the first thing to do, not the last.

The European Commission has proposed expanding CBAM scope to roughly 180 additional steel-intensive and aluminium-intensive downstream products from January 1, 2028, a change that would bring an estimated 7,500 new importers into scope and broaden CBAM toward a full value-chain instrument. Broader expansion to polymers, chemicals, and other categories is under active consideration.

The default value, and why it is the part that hurts

The charge runs off the embedded emissions of your product, the carbon released making it. Your EU importer declares that figure, and it gets priced against the EU ETS certificate rate, which the Commission posts in the CBAM Registry, quarterly through 2026 and weekly from 2027. The Q1 2026 price came in at 75.36 euros a tonne of CO2. That number moves, so check the current one rather than trusting any figure you read once.

There are only two ways your emissions number gets set. Either you supply your own verified, plant-level data, or, if you do not, the EU drops in its default value.

That default is where this stops being an abstract climate policy and starts costing you. It is built to be conservative, which is a polite way of saying it assumes you run a high-emissions process. Plenty of Indian manufacturers have spent real money on cleaner production and sit well below that default. None of it counts if you cannot prove it. Show up without verified data and you get billed as if you were the dirtiest plant in your category, whatever your factory actually looks like.

That was bad enough on its own. The definitive phase made it worse on purpose.

The transitional phase used rough global averages. The definitive phase replaced them with country- and product-specific defaults, and then added a markup that climbs every year: 10% in 2026, 20% in 2027, 30% from 2028 on. (Fertilizers run on their own schedule.) None of this is accidental. Brussels wants the default to hurt enough that you stop relying on it and start measuring. Which means the cost of not measuring is not a fixed problem you can put off. It gets more expensive the longer you wait.

The India-specific picture is already sharp. When the EU finalized its country default values in December 2025, the values confirmed for India were among the high end. Trade reporting at the time put the CBAM cost for Indian hot-rolled coil steel at over 200 euros per tonne, enough to make an otherwise competitive deal at around 510 dollars per tonne look far less attractive once the carbon cost was added.

The penalty, in other words, is not for polluting. It is for not measuring. Two factories producing the same product with the same actual emissions will pay differently if one can prove its number and the other cannot.

| Verified emissions data | No verified data (default value) | |

|---|---|---|

| Emissions figure used | Your actual, plant-level number | EU default, assumes worst-case route |

| Default value trajectory | Not applicable | Markup rising 10% in 2026, 20% in 2027, 30% from 2028 |

| Typical effect for a cleaner-than-default producer | Charged on the real, lower figure | Charged as the most carbon-intensive in category |

| Cost impact | Reflects true production | Tens of lakhs to over a crore extra per 1,000 tonnes |

| Buyer's view of you | Lower landed carbon cost | Higher landed carbon cost than a documented rival |

Industry estimates have placed the additional, avoidable cost at somewhere in the range of tens of lakhs to over a crore of rupees per thousand tonnes of product, depending on the product and the gap between the default and the real figure. For steel exporters, broader estimates suggest CBAM could require price reductions of 15 to 22 percent to remain competitive if the carbon cost is absorbed rather than documented away. For Indian aluminium exports, analysis from CEEW suggests the effective carbon cost could equal 12 to 22 percent of export value, driven by coal-based power used in smelting.

Why the cost rises even after you verify

Here is the trap for anyone who thinks measuring once and moving on settles it. There is a second escalator inside CBAM, completely separate from the default-value markup.

Right now EU factories still get most of their carbon allowances free, so in 2026 importers only pay for a sliver of the embedded emissions. As Brussels takes those free allowances away from its own producers, the slice that CBAM charges on imports grows to match:

| Year | Share of embedded emissions charged under CBAM |

|---|---|

| 2026 | ~2.5% |

| 2027 | ~5% |

| 2028 | ~10% |

| 2029 | ~22.5% |

| 2030 | ~48.5% |

| 2034 | 100% |

The steepest single jump is between 2029 and 2030, when the CBAM factor more than doubles in one year.

What this means in practice: your carbon cost is a moving target, not a fixed one. Verified data or not, the share you pay for keeps rising almost every year out to 2034. Sign a three or four year supply deal priced on 2026 CBAM exposure and you will be badly underwater by 2030. If you are quoting an EU buyer anything long-term, build the rising factor into the price, not just today's rate.

Why this is a competitive event, not just a compliance cost

Read CBAM as just another cost handed down from outside and you miss the more interesting thing it does, which is set Indian suppliers against each other.

If you can hand your buyer verified emissions data, you have turned a compliance headache into a reason to pick you. Your buyer pays a lower, accurate carbon cost on your goods. The supplier down the road who cannot produce that data saddles their buyer with the default value instead, a number that climbs every year. Put two otherwise identical Indian suppliers in front of an EU buyer and one of them now lands cheaper at the border, purely on paperwork.

Most exporters have not clocked this yet. CBAM is not only India versus Europe. It is Indian supplier versus Indian supplier, decided on who kept better records. The one who measures takes business from the one who does not, even when the two factories pollute exactly the same amount.

The timing works in favour of the documented supplier too. From the first quarter of 2027, EU importers have to hold certificates for at least half their running emissions at the end of every quarter, not just settle up once a year. That ties up their cash all year long, which gives them a reason to want suppliers whose verified, lower numbers shrink the pile of certificates they have to sit on.

And this is a race. If Vietnam or Turkey or anyone else gets their suppliers documented faster, Indian exporters who drag their feet lose ground no matter how good their factories are. First to prove their number wins, and every year of waiting costs more than the last.

What an Indian exporter should do now

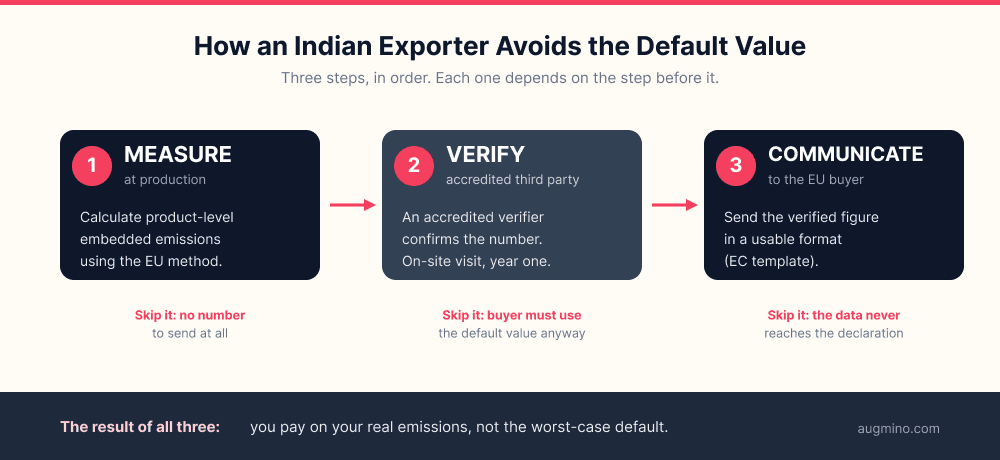

The work divides into three steps, in order. Each one depends on the one before it.

In practice:

| Step | What it involves | Who does it | When to start |

|---|---|---|---|

| 1. Measure | Calculate product-level embedded emissions using the EU methodology, mapping the energy and process inputs for the covered product | Internal team, often with a consultant for the first cycle | Now |

| 2. Verify | Have the emissions data confirmed by an accredited third-party verifier so it is accepted in place of the default value | Accredited verification body | Once the first measurement exists |

| 3. Communicate | Deliver the verified figure to the EU buyer in a format their importer can enter in their CBAM declaration | Exporter to buyer | Before the buyer has to ask |

Measure first. You need the embedded emissions for the actual products you export, calculated at the plant, using the EU's prescribed method. This is not a glossy sustainability statement. It is a specific, product-level number built from the real energy and process inputs that go into the part. If you have never done it, the first calculation is the painful one, because it forces you to map exactly what goes into making the thing. After that it gets easier.

Then verify. Your number only beats the default value if an accredited third party signs off on it. In the first year that means an on-site inspection, so this cannot be done purely on paper from a desk. Line up a verifier and find out what they will want to see early, well before a buyer puts you on the spot.

Then hand it over. The verified figure has to reach your buyer in a shape their importer can drop straight into the CBAM declaration. The Commission publishes a standard template for exactly this. A perfect emissions number sitting in a folder at your factory protects you from nothing; it has to travel.

One break worth tracking. If a carbon price was already paid back home during production, CBAM lets the importer knock that off what they owe. From 2027 the Commission will publish reference carbon prices for countries that run a pricing scheme, and declarants can use those to claim the reduction. India's own Carbon Credit Trading Scheme started its compliance phase in 2026, so the hook exists. The catch is that, as of 2026, the EU has not finalised how a price paid in India gets recognised and counted, so do not bank on an automatic offset yet. Worth watching closely, though, because if it lands it takes real money off the bill for anyone already in the Indian scheme.

CBAM is not only an EU story

The EU got there first, but it is not the only game anymore. If you sell into more than one Western market, plan for several of these at once rather than fighting them one at a time.

The United Kingdom is next in line. Its CBAM starts January 1, 2027, covering aluminium, cement, fertilisers, hydrogen, and iron and steel. The mechanics differ from the EU's: it is a straight tax, not a certificate system, with rates set quarterly off the UK ETS price. There is a registration threshold of 50,000 pounds of CBAM goods over twelve months, no reporting trial period, and indirect emissions are held back until at least 2029. Like the EU, it gives credit where an overseas carbon price was already paid. Supply both EU and UK buyers and 2027 lands you two separate carbon border regimes at once, each with its own rules.

Others are circling. Canada, the US, Australia, Taiwan, and Turkey are all either drafting or seriously weighing their own carbon border measures. In the US, border-carbon bills have come from both parties, though nothing federal has actually passed yet. Some developing economies are moving from the opposite end, standing up or speeding along their own domestic carbon pricing so the revenue stays home instead of getting scooped up at the EU border. Morocco's phased carbon tax, starting January 2026, is a supplier country doing exactly that to keep its exporters in the game.

For planning, the exact shape of each scheme matters less than the direction of travel. The work you do for EU CBAM, measuring emissions, getting them verified, packaging the documentation a buyer can use, is the same work the UK CBAM wants, and most of what comes after it. You build it once and reuse it. That, more than any single deadline, is why it pays to start now instead of waiting for each border to catch fire on its own.

The underlying pattern

Take the carbon out of it and CBAM rewards the thing global buyers have always rewarded: a supplier who can prove what they do in a form the buyer can use. A factory that can document its emissions to an outside standard is almost always a factory that can document everything else, the material certificate, the first article report, the quality trail. It is the same discipline wearing a different label.

All CBAM has really done is put a big, specific, rising price tag on that discipline. Have it, and you have an edge that compounds. Lack it, and you get a bill built on a number that was never yours, climbing a little higher every year you put off fixing it.

See Also

Frequently asked questions

What is CBAM and when did it start?

CBAM is the EU's Carbon Border Adjustment Mechanism, a regulation that places a carbon price on imported carbon-intensive goods to match what EU producers pay under the Emissions Trading System. It began as a transitional reporting phase in October 2023 and entered its definitive phase, with real financial obligations and mandatory verification, on January 1, 2026. Certificate sales open February 1, 2027, and the first annual surrender deadline is September 30, 2027.

When does an Indian exporter actually start paying?

The exporter does not pay CBAM directly; the EU importer does. But the cost attaches to goods imported from January 1, 2026 onward. The importer buys and surrenders certificates for 2026 imports in 2027, with the first surrender due by September 30, 2027. Because the importer's cost depends on whether your verified emissions data is available, the practical timeline for the exporter is now: the data has to be generated at the point of production, well before any certificate is bought.

Which products does CBAM cover, and is there an exemption?

The definitive phase covers iron and steel, aluminium, cement, fertilizers, hydrogen, and electricity. Whether a specific product is in scope is determined by its CN customs code. Importers whose total annual imports of CBAM goods do not exceed 50 tonnes are exempt, which the Commission says covers about 90% of importers while still capturing 99% of embedded emissions. Electricity and hydrogen are excluded from this exemption. Coverage is proposed to expand to around 180 additional downstream products from 2028.

What is the CBAM default value and why does it matter?

When an exporter cannot provide verified emissions data, the EU applies a default value to calculate the carbon cost. The default assumes a high-emissions production route. In the definitive phase, these default values are country- and product-specific and carry a markup that rises by 10% in 2026, 20% in 2027, and 30% from 2028 onwards for most goods. This escalation is explicit policy designed to penalise non-measurement, so the cost of relying on the default value increases every year.

How much can the default value cost an Indian exporter?

The cost depends on the product and the gap between the default value and the exporter's real emissions. Industry estimates place the additional, avoidable cost in the range of tens of lakhs to over a crore of rupees per thousand tonnes for some products. When the EU finalised country default values in late 2025, the CBAM cost for Indian hot-rolled coil steel was reported at over 200 euros per tonne. For steel broadly, estimates suggest price reductions of 15 to 22 percent may be needed to stay competitive if the cost is absorbed; for aluminium, CEEW estimates the effective carbon cost could reach 12 to 22 percent of export value.

Does the cost stay the same once I have verified data?

No. Separate from the default-value markup, CBAM is phased in as the EU withdraws the free allowances its own producers receive. The share of embedded emissions that CBAM charges rises from a small fraction in 2026 to 100% by 2034, with the steepest jump between 2029 and 2030. Even with verified data, the proportion of carbon you pay for grows almost every year, so multi-year contracts to EU buyers should model the rising CBAM factor rather than today's rate.

How can an Indian manufacturer avoid the default-value penalty?

Three steps. Calculate your product-level embedded emissions using the EU's method, get that data verified by an accredited third party (an on-site inspection is required in the first year), then pass the verified figure to your EU buyer on the Commission's template so their importer can use it in the declaration. Start the measurement now, because the data has to come from the point of production no matter when the payment falls due.

Does CBAM affect competition between Indian suppliers?

Yes. Faced with two comparable Indian suppliers, an EU buyer has a growing financial reason to prefer the one who can provide verified emissions data, because it results in a lower, accurate carbon cost. From 2027, importers must hold certificates for at least 50% of their emissions at each quarter-end, which adds a cash-flow reason to prefer documented suppliers throughout the year. CBAM sorts suppliers by measurement discipline, so the manufacturer who measures can win business from one who does not, even when their actual emissions are identical.

Does CBAM apply only to the EU?

No. The United Kingdom introduces its own CBAM on January 1, 2027, covering the same core sectors but operating as a direct tax rather than a certificate system, with a 50,000 pound registration threshold and indirect emissions delayed to 2029. Beyond the UK, governments including Canada, the United States, Australia, Taiwan, and Turkey are defining or exploring similar measures, and some supplier countries such as Morocco are introducing domestic carbon pricing to keep the revenue at home. The emissions measurement and verification infrastructure built for EU CBAM is largely portable to these other schemes, which is a further reason to start now.

Ready for fewer, better conversations?

Augmino connects verified Indian manufacturers with buyers who mean business.

Apply to Join